Adhila Mayet and Caitlin Japhet attended a GreenPeace conference where they launched and discussed their report on “Shopping Clean – Retailer and Renewable Energy”. Five of South Africa’s largest retailers were assessed and ranked according to their performance, with respect to sustainability. The five retailers were Woolworths, Massmart, Pick ‘n Pay, Spar and Shoprite, with Woolworths (Justin Smith) and Massmart (Alex Haw) representatives present on the panel. The other panellists were Ayanda Nakedi (Head of Eskom Renewable Energy Unit), Mr Mike Levington (Vice Chair of SAPVIA), Melita Stele (Green Peace) and Dr Tobias Bischoff-Niemz(CSIR).

Melita Stele opened the floor with discussions around how the retailers were scored and why they were ranked accordingly. She discussed the barriers to successful roof top PV with the largest barrier being legislation and what the retail sector’s role in a South African energy revolution is. She compared Renewable Energy and the retailers’ role in it, to the Parkhurst suburb and their role in catalysing the roll-out of fibre to home. She closed with recommendations for the way forward.

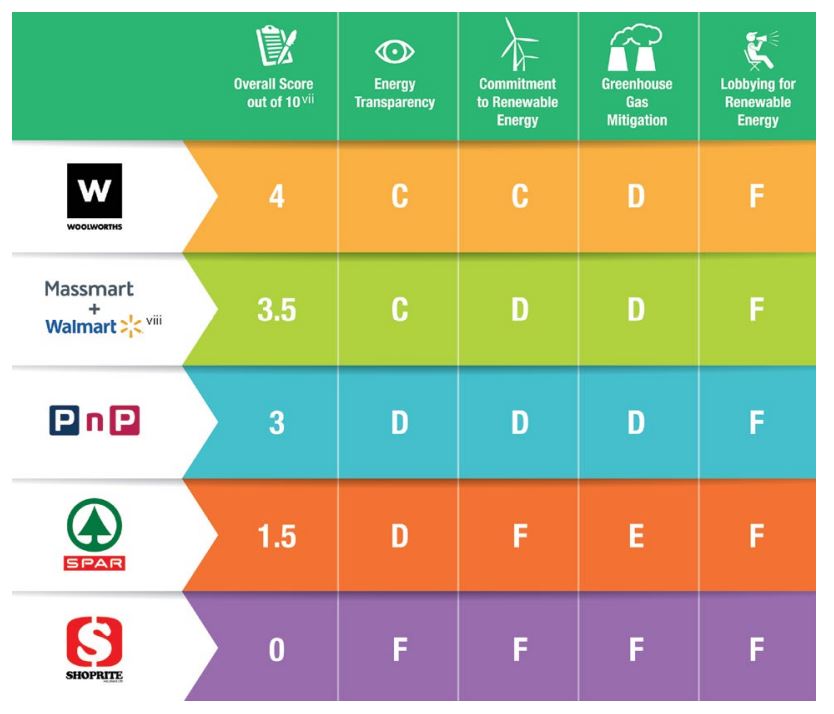

The retailers were appointed an overall score out of 10, which was calculated by assessing four separate categories; energy transparency, commitment to renewable energy, greenhouse gas mitigation and lobbying for renewable energy. Each category was scored out of ten in alphabetical order with A being the highest and F the lowest. See the info-graphic below.

As can be seen, the overall scores were very low, with the highest from Woolworths, being 4/10. Melita noted that this was mainly due to the lack of active lobbying for renewable energy across the board. Woolworths topped Massmart with their commitment to Renewable Energy as they plan to announce, on the 16th of May, their commitment to 100% Renewable Energy by 2030. They as yet do not have a structured plan and hence did not attain a higher score.

As can be seen, the overall scores were very low, with the highest from Woolworths, being 4/10. Melita noted that this was mainly due to the lack of active lobbying for renewable energy across the board. Woolworths topped Massmart with their commitment to Renewable Energy as they plan to announce, on the 16th of May, their commitment to 100% Renewable Energy by 2030. They as yet do not have a structured plan and hence did not attain a higher score.

Justin Smith from Woolworths took the floor discussing their efforts around being sustainable. Woolworths has been working on energy efficiency programs for the last 10 years and have an onsite target of 2MW for the head offices and main distribution centre. They pledged to only invest in buildings in the future, which are solar powered. At this stage they do not own a single one of their outlets. This was a major barrier noted by the retailers and reiterated by Massmart, that they do not own many of their stores and hence do not have control of installing Solar on the roof tops. He noted that retailers need to understand their influence better in terms of lobbying as well as influencing their supply chain to go green.

Alex Haw from Massmart announced the commissioning of their first Solar PV plant the day before (19th of April 2016). This is a 572kVA solar PV plant on one of their Macro stores with a second one to be commissioned on the Macro Woodmead store (700kVA) before the end of the year. Alex noted the importance of understanding your baseline, reducing your overall consumption through energy efficiency and then beginning to install Solar PV.

Dr Tobias from the CSIR had a very interesting view on the levelised cost of energy (LCOE) for renewables. He noted that the current Eskom price is not reflective of the system in place, as it will soon need to be rebuilt. One needs to compare the new build price of energy in the country to the LCOE and not the current Eskom prices, which will be short lived. We need to look to the future as a country and the government needs to assess installing a mix of Renewable and baseload energy supply as an alternative to building new coal-fired power stations. He noted that RSA is in a unique position to look at the energy supply of the country with Renewable Energy as a business solution on the Macro-economic system.

The CSIR have recently completed a study on the wind energy potential in the country with the conclusion that wind potential in the country is completely on par with solar with 80% of the land mass having a load factor of 30% or higher which presents a firm business case for the technology.

Mike Levington from SAPVIA spoke of the importance of the codes, standards and legislation around installing Solar PV systems. SAPVIA was initiated in 2010 and has more than 160 members. Mike commented that SAPVIA is ready for the roll-out of renewable energy across the country and that legislations have been written but is still under review. He is hopeful that they will be published by the end of the year. In 2015, 130MW of roof top solar PV was installed across the country, with an industry target of 170-200MW to be installed in 2016. He noted the influence that industry has on governmental bodies and that the fact that industry has gone ahead and installed Solar PV systems has created pressure on the government to react and publish codes and standards to control the industry boom.

Eskom’s Ayanda Nakedi heads the renewable division in the utility, and presented a bit of a reality check in terms of renewable energy in South Africa. She stressed that more needs to be done to solve the challenges – specifically the fact that both wind and solar energy do not provide “baseload” energy. Essentially, embedded renewable generation turns Eskom’s grid into a back-up solution. This does not bode well for its revenue, given that lucrative peak and standard tariffs generally occur during the day when solar and wind generators produce most of their power. The evolution of the consumer of electricity into a “prosumer”, who also produces its own power, poses a threat to the state-owned entity’s current revenue model. With that said, Eskom recognises the importance of renewable energy and has just commissioned its own wind farm, and is in the process of commissioning one of the largest concentrated solar power (CSP) plants in the country.

An interesting question posed to the panellists was “What are the top two items on your policy / regulation wishlist for renewable energy?” This followed the clear consensus that regulation on renewable energy is lagging in the embedded generation space. The most common answer, voiced specifically by Haw of Massmart, was the introduction of feed-in-tariffs to improve the business case of solar power for individuals and organisations alike. Bischoff Niemz’s answer provided a longer-term and more visionary solution; the transport of power should be separated from the utility, to remove the burden of maintaining the network for power that may not be purchased from Eskom. Another shared view amongst the panellists was the utter importance of updating the Integrated Resource regularly and deliberately, with constant feedback from the market.

Regulatory environment aside,both retailer representatives present expressed their frustration that most of their stores are leased and not owned. The decision to go renewable lies with the property owners and developers rather than the retailers, who are merely tenants. Steele challenged Massmart and Woolworths to use their undoubtable bargaining power as big brands to influence the property owners to go renewable. Woolworths and Massmart agreed that working together is crucial, especially in newer malls where there are as many as six anchor tenants and leverage is diluted amongst several retailers.

In closing, everyone agreed that whilst there are many challenges in the embedded renewable generation industry in South Africa, bold commitments and actions are required. GreenPeace reminded the audience and panellists that although change can be incremental and gradual, sometimes one needs to “knock down the door” and demand change. The difficult but exciting question of what the future of SA’s energy market looks like drew a range of answers across the board. Whilst the CSIR predict a 30% drop in PV tariff’s over the next five years, SAPVIA worried about the impact of the impending boom of electric cars will mean for our consumption as a nation. A member of the audience compared renewables in the electricity market to disruptive companies like Uber and AirBnB in stable, developed markets. Some are excited about the future of batteries and storage as a means to solving the baseload challenges, whilst others are waiting eagerly to see how prosumers restructure our demand and usage patterns. As a group, the sentiment was clearly enthusiastic, excited, and raring to go in the world of renewables.

Written by: Caitlin Japhet & Adhila Mayet